About This Client

This is a very common factoring lead that became a client for this “referrer”. Small business “service companies” are one of the most productive types of companies for new brokers to “cut your teeth on”. Many of these companies are not able to access traditional bank funds and to finance their growht, they will often need to explore other alternatives such as factoring. When talking “marketing”, successful brokers and consultants view this cleints as “low-hanging fruit”.

Sourcing This Client

Millie Stubblefield was a receptionist at a local bank in Lake Mount City, KY. As a bank employee she belonged to the local Chamber of Commerce and would periodically recruit those she met socially at the Chamber to the bank for loans and other services.

One day, she was pleasantly surprised to see a new Chamber acquaintance walk in the bank to apply for a business loan. The business owner had previously told her that his company, a condominium maintenance provider, was having some cash flow trouble and unless he could get a loan, he might have to lay off some employees and downsize a bit. Millie told him to stop by the bank and they would see what they could do.

Mille introduced the business owner to one of the bank’s loan officers but unfortunately, there was little help the bank could provide. The business owner had poor credit and no collateral for a loan. The problem he was having was one of cash flow caused by his slow paying customers (management companies) which were taking 60 days or longer to pay for his services. As the business owner was leaving, Millie stopped him and gave him a phone number to call. It was the number of a local factor who had made a factoring presentation to the bank’s employees earlier in the year. Millie thought factoring just might be the solution for this business.

Later that day the business owner placed a call to the factor who immediately set up an appointment. It was clear that the business owner’s cash flow problem was being caused by the slow paying management companies and that factoring would provide a ready solution. Each week, the factor would purchase the maintenance company’s invoices with an up-front 80% cash advance. The factor would then wait to get paid in 60 days. Once paid, the factor would remit the remaining 20% less a 5% fee for its factoring services.

With over a 40% profit margin, the maintenance company’s owner could easily absorb the factoring costs. He would now receive payment within hours of completing his work and his customers could still enjoy their 60 day payment terms…all because of factoring.

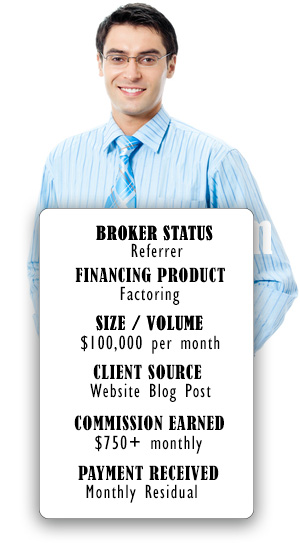

For Millie, there was an added bonus. Although she did nothing more than provide a phone number that resulted in a new client being added to the factor’s portfolio, she was now the broker of record for that referral and would be entitled to a monthly commission check. The maintenance company was generating about $100,000 in billings each month. As the broker of record Millie would receive 15% of the factoring fees earned on financing those billings or about $750 per month. Additionally, she would receive those checks for the life of the account which is typically 5 years or longer. This could represent a total income package of over $45,000…FOR ONE REFERRAL!

While it is certaily not free to subscribe as a member at your local Chamber of Commerce, it should always be a marketing goal if you are seeking a “professional” career in factoring and small business finance. Additionally, use you LinkedIn membership to connect with as many local lending officers in your community.